July 28, 2025

Hydrogen Got a Reprieve in the Reconciliation Bill, but It Needs More Than That to Be Cost Competitive

By Abbe Ramanan

Utilities in at least 18 states are developing “hydrogen-ready” combined cycle (CC) or combustion turbine (CT) power plants. These plants are part of a larger shift towards maintaining a reliance on fossil fuel infrastructure, both by building new plants and keeping old ones online, spurred by a pro-coal and gas administration and fearmongering around grid reliability concerns.

Thanks to extensive lobbying from industry groups as well as high-level Republican lawmakers, the budget reconciliation bill passed on July 4 left the 45V Clean Hydrogen Production Tax Credit nearly intact, at least compared to wind and solar production tax credits. The 45V tax credit, which was originally slated to last for the next 10 years, now terminates in 2028. Projects must begin construction by 2027 to be eligible for the credit. The bill did contain some good news for hydrogen fuel cells, which will now be eligible for the Section 48E credit. The bill also removes previous restrictions which would have required eligible fuels to be emissions neutral, meaning hydrogen fuel cells running on carbon-intensive blue or grey hydrogen will now be eligible for the 48E tax credit. The reconciliation bill might spell bad news for the green hydrogen industry, but the 45V tax credit was never going to make hydrogen an affordable choice for power generation.

A new report published by Clean Energy Group (CEG) in partnership with Current Energy Group conducts a levelized cost of storage (LCOS) analysis on hydrogen, particularly hydrogen peaker power plants, compared to other forms of long duration energy storage (LDES) technologies.

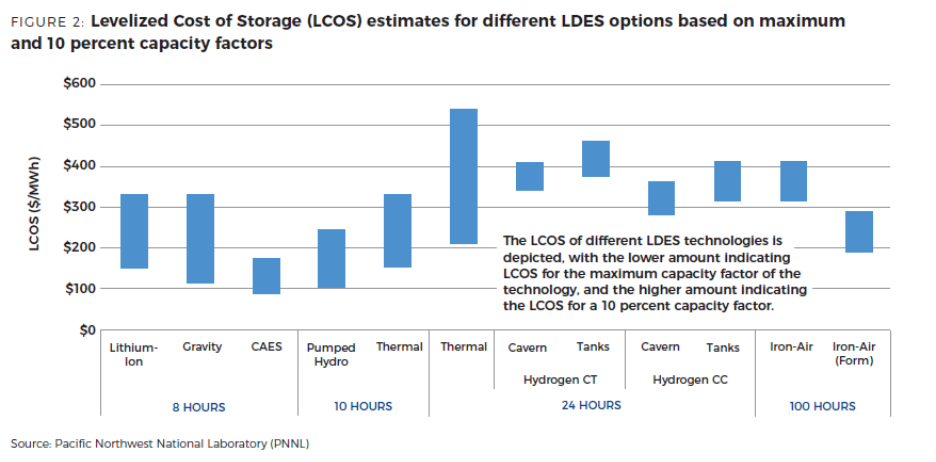

The analysis detailed in the report is clear: while hydrogen might have some competitive edge when it comes to very long duration seasonal storage, hydrogen power plants are expensive and unnecessary for shorter durations. This is especially true in the 8–10-hour duration range, also known as medium duration energy storage (MDES).

Some of this is due to the nature of hydrogen and hydrogen power plants. Due to the inefficiencies associated with hydrogen production and the high operating costs of power plants, hydrogen use in power plants does not make sense for day-to-day power generation. Thus, most hydrogen power plants are likely to operate as peakers, only coming online for a few hours at a time during periods of high demand. In the figure above, the higher range represents the LCOS of various technologies operating at a 10 percent capacity factor, analogous to a peaker plant. Pumped hydropower and thermal storage both outperform hydrogen in the MDES category (10 hours). In the next 10 years, MDES resources will be much more critical for grid balancing and reliability. When looking at longer, multi-day durations, iron-air batteries can potentially outperform hydrogen power plants, although there is a wide range of LCOS estimates for iron-air batteries. Multi-day storage is unlikely to be widely needed for grid stability in the next decade.

The LCOS analysis includes the 45V credit in the hydrogen price, as well as the 30 percent Investment Tax Credit (ITC) in the cost for the other LDES technologies. After 2027, the LCOS for hydrogen technologies will likely increase, particularly for hydrogen power plants, which unlike fuel cells are ineligible for 48E. However, even hydrogen fuel cells are not competitive with other technologies in an MDES context.

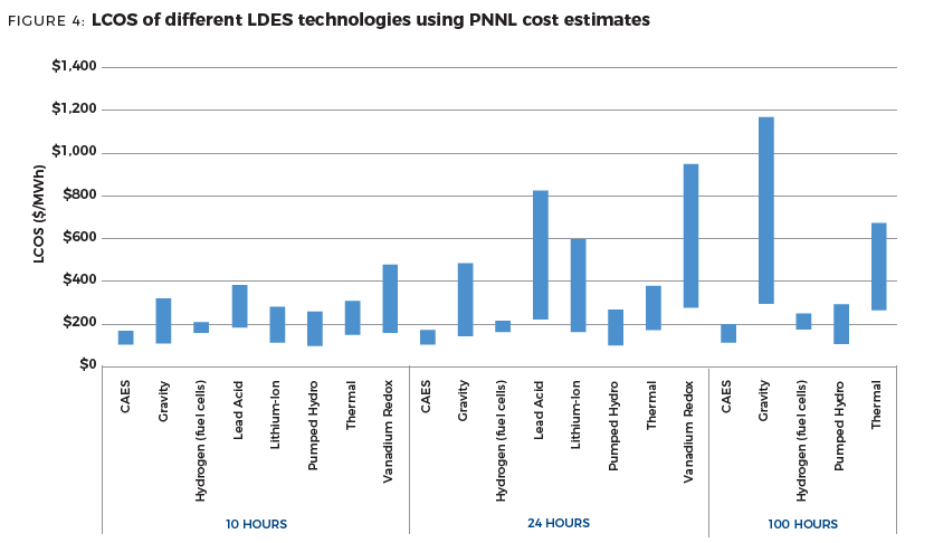

As seen in the chart above, compressed air energy storage (CAES) and pumped hydro technologies present the lowest LCOS across all duration categories. Gravity storage also exhibits the potential for a low LCOS for 10-hour duration storage. Lithium-ion battery technologies are excluded from the longer duration categories, as their costs scale directly with duration, and thus are expensive options for longer durations. However, for MDES, lithium-ion batteries, CAES, pumped hydro, and gravity storage all have the potential to be more cost-competitive than hydrogen fuel cells.

Outside of cost, green hydrogen production and use also has the potential for significant harm to public health and the environment, including contributing to global warming, draining local water supplies, weakening pipeline infrastructure, and contributing to significant emissions of the harmful air pollutant nitrogen oxide. These issues are compounded when looking at other forms of hydrogen production that are reliant on fossil fuels. These harms will not be mitigated by improvements to technology over time, making it imperative that utilities accurately model the true impact of these technologies in resource planning processes.

There’s no reason to build hydrogen power plants today, particularly when other LDES technologies can meet the same needs with fewer costs and harms. Even with 45V, hydrogen was never going to be cost-competitive. The reconciliation bill has only widened the competitiveness gap between hydrogen and other energy storage technologies, many of which will maintain eligibility for the 30 percent ITC through 2032.

The hydrogen industry may have been given a reprieve in the reconciliation bill, but it was never competitive to begin with.