September 3, 2025

What Nonprofits Need to Know about the Investment Tax Credit in 2025

By Anna Adamsson

In the July 2025 “One Big Beautiful Bill Act,” Congress terminated key aspects of the Investment Tax Credit (ITC) for solar and wind projects and created barriers for projects pursuing energy storage and other zero emissions technologies. Under the revised ITC guidelines, solar and wind projects must begin construction by July 4, 2026, or be placed into service by December 31, 2027, in order to be eligible to receive the ITC.

This post will provide a brief overview of the ITC and describe how solar, storage, and wind projects can still access the ITC, including Direct Pay and bonus credits.

What is the Investment Tax Credit?

The ITC allows US taxpayers to deduct a specific percentage of renewable energy project expenses from their federal taxes. It has been instrumental in building the renewable energy market in the US, making clean energy technologies more affordable as the market has matured. The ITC was first established in 2005, and it has been expanded and extended many times since then. The biggest expansion of the ITC was in 2022 with the passage of the Inflation Reduction Act (IRA). Notably, the 2022 expansion contained a provision that allowed nonprofits, which do not have a tax burden, to access the full value of the ITC through a provision called Direct Pay. In a previous blog, Clean Energy Group provided an overview of IRA changes to the ITC and offered guidance for nonprofit organizations seeking to install and own clean and resilient power technologies.

The IRA updated and expanded the ITC for solar and battery storage resilient power projects. The ITC, which was previously set at a 26% credit for 2023 and a 10% credit for every year after that, was raised to cover 30% of the eligible project installation costs through 2032. This change significantly increased the anticipated savings for solar projects and was intended to help create stability in the market over the next decade.

Congress also expanded the ITC in three crucial ways: 1) Nonprofits with no tax liability can apply for Direct Pay reimbursement equal to the value of the tax credit, 2) Storage-only projects are eligible for the ITC, and 3) The ITC includes several “bonus credits” that can significantly increase savings for projects serving low-income and underserved communities.

As mandated by the IRA, in January 2025, the Energy Investment Tax Credit (Section 48) was replaced with the technology-neutral Clean Electricity Investment Credit (Section 48E), which expanded the ITC to cover any technology that generates electricity with net-zero emissions. This post will refer to the updated 48E ITC.

What kind of clean energy technology is eligible?

Currently, ITC eligible projects must generate electricity with a greenhouse gas emissions rate that is less than or equal to zero, such as solar and wind. Qualified energy storage technologies are also eligible.

Energy storage, as defined in 26 U.S. Code §§ 48E(c)(2) and 48(c)(6), includes “property … which receives, stores, and delivers energy for conversion to electricity … and has a nameplate capacity of not less than 5 kilowatt hours.” It does not include storage that is “primarily used in the transportation of goods or individuals and not for the production of electricity.”

How much is the ITC worth?

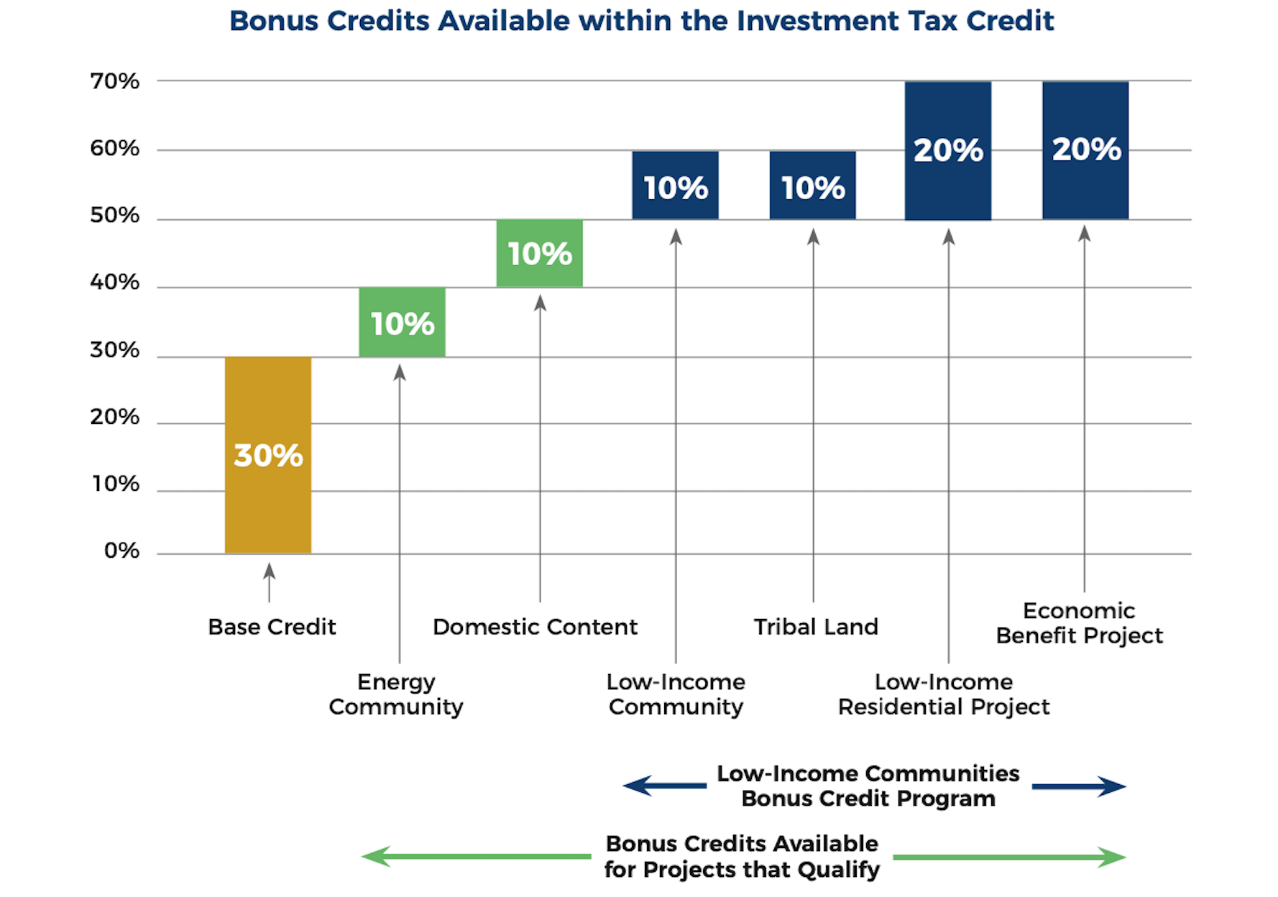

The ITC provides a 30% baseline credit for projects under one megawatt capacity and for larger projects that meet prevailing wage and apprenticeship requirements. Projects may be eligible for up to six bonus credits that could raise the value of the ITC up to 70% of the eligible costs from the project’s installation.

What is the status of the Investment Tax Credit in 2025?

Solar, storage, and other eligible projects can still access the ITC. The deadline to begin and complete construction (or be “placed in service”) has been updated and differs between solar, wind, and storage projects. The Treasury Department is expected to release additional guidance establishing new Foreign Entity of Concern (FEOC) requirements that will impact all projects.

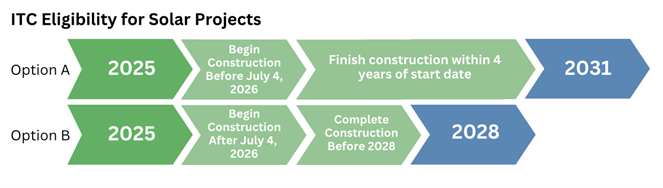

Solar projects that begin construction before July 4, 2026, are eligible to receive the ITC. Current guidance from the Internal Revenue Service (IRS) states that entities have four years from the start of construction to complete the project and claim the tax credit; however, the IRS may issue updated guidance restricting the construction timeline. Projects that begin construction after July 4, 2026, are still eligible for the ITC if those projects complete construction and are operational by December 31, 2027. These timelines also apply to onshore wind projects (offshore wind follows different commence construction regulations).

Storage projects can continue to access the full ITC through the end of 2033. The ITC begins to phase out in 2034 and 2035. Although the ITC will remain available for another decade, starting in 2026, storage will be subject to additional FEOC restrictions. These updates to the ITC also apply to geothermal, hydrogen, and nuclear technologies.

Beginning of Construction Standards: Projects typically are considered to have begun construction when either 1) significant physical work begins, subject to the “physical work test” or 2) five percent or more of the project has been paid for following the “five percent safe harbor” standard.

Updated guidance (Notice 2025-42) from the Treasury Department removes the “five percent safe harbor” for solar projects that are larger than 1.5 megawatts and all wind projects. To remain eligible for the ITC, those projects must meet the physical work requirement standard regardless of how much project funding has been expended. The “physical work test” can be passed if “significant” work has ensued, such as the installation of racks or other support structures (on-site) or the manufacturing of components (off-site). This does not impact solar projects smaller than 1.5 megawatts or solar projects that will be operational before 2028.

The updated guidance does not impact energy storage projects or other tax credit-eligible technologies. Importantly, the Treasury Department noted that it may release additional guidance about what constitutes the ‘beginning of construction’ specifically for projects seeking to avoid new FEOC restrictions in 2026. To learn more, view the Tax Law Center’s guidance.

Foreign Entity of Concern Restrictions: Beginning in 2026, all clean energy projects (including solar, storage, and wind) will be subject to new FEOC restrictions. As it currently stands, the rule limits the use of materials or components produced by Prohibited Foreign Entities (PFEs), such as in China, Iran, North Korea, and Russia. If the ratio of materials produced by PFEs exceeds allowed amounts for the given year (determined by the “material assistance cost ratio”), then the project will not be eligible for the ITC. Under the FEOC rules, projects can also not be owned by a PFE or disburse payments to a PFE. Projects that begin construction by the end of the year (December 31, 2025), will not need to abide by FEOC requirements. The New York University Tax Law Center published this resource detailing the new FEOC/PFE requirements.

Can nonprofits benefit from the Investment Tax Credit?

Importantly, the ITC still benefits everyone, not only those that have tax liability. Nonprofits and other tax-exempt entities, like municipalities and Tribal governments, are eligible to receive the ITC in the form of a direct pay reimbursement.

Direct Pay, also referred to as Elective Pay, enables tax-exempt entities to receive payment equal to the full value of the ITC and its bonus credits after a clean energy project has been “placed in service.” To participate in Direct Pay, tax exempt entities must alert the IRS in that year’s tax return and through the IRS pre-filing registration form.

Clean Energy Group published the guide “What Nonprofits Need to Know When Applying for Direct Pay” to help tax-exempt entities navigate the key steps to receiving direct pay reimbursement. The guide also includes a customizable timeline, which makes it easier for projects to track progress through those steps and ensure that no deadlines are missed.

To learn more about the Direct Pay process and project eligibility, view the Direct Pay Fact Sheet.

What is the status of Direct Pay in 2025?

Tax-exempt entities can still access the full value of the ITC through Direct Pay. Congress did not materially change the Direct Pay provision; however, its existence relies upon the availability of the underlying tax credits. Under the current law, as long as your project is eligible for the ITC, it will be able to access Direct Pay reimbursement.

What are the Bonus Credits?

The ITC includes six different bonus credits that projects may apply for. Four of those credits are housed within the Low-Income Communities Bonus Credit Program. Projects can only apply for one of the four bonus credits within the Low-Income Communities Bonus Credit Program. This means a project could either receive a 10% or 20% bonus credit, depending on their eligibility.

The four bonus credits within the Low-Income Communities Bonus Credit Program (§ 48(e)) are:

- 10% bonus for projects located in a low-income community

- 10% bonus for projects located on Tribal land

- 20% bonus for projects when the facility is part of a qualified low-income residential project

- 20% bonus for projects when the facility is part of a qualified low-income economic benefit project

The two stackable bonus credits (§ 48) are:

The ITC also includes two additional 10% credits, which are stackable. Projects that are eligible can apply for both bonus credits, in addition to the 30% baseline credit and one of the bonus credits within the Low-Income Communities Bonus Credit Program.

- 10% bonus for projects located in an “energy community” (mapping program indicating potential eligibility)

- 10% bonus for projects that meet domestic manufacturing requirements

Learn more about each of these six bonus credits in a series of fact sheets. To read about the application process for the Low-Income Communities Bonus Credit Program, view this post.

What is the status of the Bonus Credits in 2025?

Projects can still apply for the Bonus Credits in 2025. Congress did not materially change the Bonus Credit program; however, like Direct Pay, its existence relies upon the availability of the ITC. Under the current law, as long as your project is eligible for the ITC, it can proceed through the existing process to apply for one or more bonus credits.

The requirements to receive Domestic Content bonus credits were adjusted. Based on the currently available information, projects that begin construction through 2025 must ensure at least 45 percent of their components are produced domestically, rising to 50 percent in 2026, and 55 percent for future years (offshore wind projects are subject to separate benchmarks).

What is the application process like for these incentives?

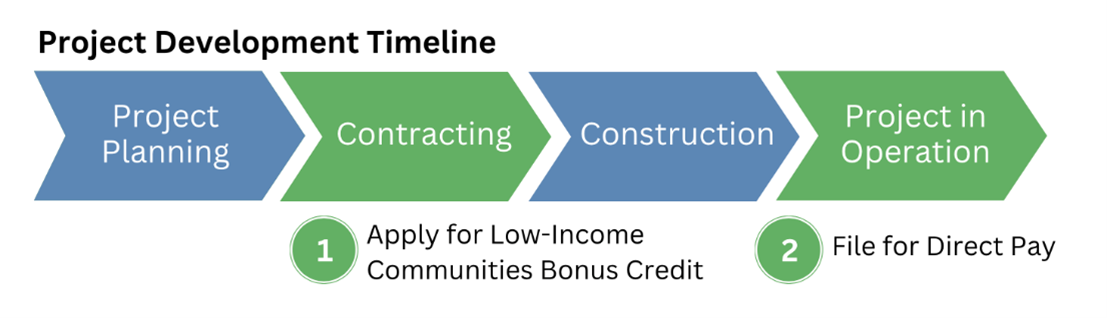

The ITC baseline credit and Direct Pay are not subject to competitive application cycles. Instead, all eligible tax-exempt entities that meet the requirements for the ITC and that file appropriately will receive the ITC through Direct Pay. Projects must file for Direct Pay after the clean energy project has been “placed in service,” which is shown in Step 2 of the Project Development Timeline figure below. Learn more about the process to apply for Direct Pay in this guide.

Although the ITC and Direct Pay are available to all eligible projects, the four bonus credits within the Low-Income Communities Bonus Credit Program only have limited annual capacity. Eligible project teams can apply for a “capacity allocation” once they have a contract in place for the project, indicated in Step 1 of the Project Development Timeline figure. Projects may also need additional documentation depending on which of the bonus credits the project is applying for. The project team must apply for and receive a capacity allocation before the project has been placed in service. Learn more about the application process for the Low-Income Communities Bonus Credit Program in this post.

Resource Library

Investment Tax Credit Accelerated Phaseout

In July 2025, the federal government moved to eliminate the Investment Tax Credit for solar and onshore wind projects that begin construction after July 4, 2026 (or that are not operational before 2028). To learn more about the recent updates and their impact on community-led project development, visit:

- Clean Energy States Alliance Diagram of Key ITC Deadlines

- Lawyers for Good Government Fact Sheets and Guidance Briefs

- Clean Energy Group Updates to the ITC Fact Sheet

Residential solar projects are subject to a more accelerated phaseout. Homeowners must have installed and commissioned their solar systems before the end of 2025 to still qualify for the Investment Tax Credit.

Direct Pay for Tax Exempt Entities

Tax exempt entities and governmental entities are able to access the ITC and its bonus credits through Direct Pay reimbursement, also referred to as Elective Pay. To learn more about the Direct Pay option and the process to receive Direct Pay reimbursement, visit:

- Clean Energy Group Direct Pay Fact Sheet

- Clean Energy Group Direct Pay Guide for Nonprofits, which includes an in-depth look into the application process and access to a customizable application timeline

- Lawyers for Good Government: Elective Pay & IRA Tax Incentives Resources Page

- IRS Elective Pay and Transferability webpage, which links to relevant resources and fact sheets

- IRS Elective Pay Frequently Asked Questions

Investment Tax Credit and its Bonus Credits

Clean Energy Group and the Clean Energy States Alliance published several blog posts and resources about the updates to the ITC and the impact of the IRA including:

- Investment Tax Credit Fact Sheets: Bonus Credit Program

- Low-Income Communities Bonus Energy Investment Credit Program: Answers to Frequently Asked Questions

- How to Make the Most of the Investment Tax Credit: Applying for Bonus Credits

- Carveouts within the Low-Income Communities Bonus Credit Program Prove Meaningful, but Underutilized

- The Inflation Reduction Act Offers Powerful Tools for Solving the Peaker Problem

- The Inflation Reduction Act is a Game Changer for Nonprofits Seeking Solar+Storage

What if I have more questions?

You can reach out to Anna Adamsson from Clean Energy Group ([email protected]). Clean Energy Group and its employees are not tax advisors. Projects should seek professional tax advice before making decisions.

Visit the Treasury Department’s webpage for an update-to-date index of all notices and procedures published on IRA-related tax incentives and policies including Direct Pay, the Clean Energy Tax Credit (§ 48E), the Low-Income Communities Bonus Credit Program (§ 48(e)), and the bonus credits for energy communities and for domestic content. The IRA (Public Law No: 117-169 (8/16/2022)) lays the groundwork for each of these programs and the 2025 One Big Beautiful Bill Act updated and accelerated the phaseout of the ITC.